Loans are typically seen as the last option, associated with financial trouble or terrible money management. In Nepal, the concept of taking a loan often carries a negative connotation. However, it's time to reevaluate the negative perceptions attached to loans. Taking out a loan isn't inherently a bad decision or a sign of financial distress. In fact, it can be a strategic move towards achieving financial goals or addressing urgent needs. Whether it's for starting a business, investing in education, or covering unexpected expenses, loans provide a crucial financial lifeline. Moreover, loans can become essential for seizing opportunities and dealing with money problems.

Having said that, loans can be a strategic move but they also come with risks if you don't plan and manage them carefully. Thus, understanding the terms, managing repayments responsibly, and utilizing the funds wisely can turn a loan into a valuable tool. By reframing our perspective on loans, we can unlock the potential to drive progress and prosperity. Let's explore why taking a loan can actually be a prudent decision and sheds light on common misconceptions surrounding borrowing money.

In the world of finances, loans often get a negative review due to some common misconceptions. In reality, loans can be strategic tools for achieving goals or handling unexpected expenses. Here are the common misconceptions about loans:

Contrary to popular belief, taking out a loan doesn't necessarily indicate financial distress. Many financially savvy individuals utilize loans as part of their wealth-building strategy, leveraging borrowed funds to generate returns and expand their financial portfolios. Thus, loans can also be used strategically to achieve goals or handle unexpected expenses without indicating financial instability.

Although it's true that poorly managed debt can result in a never-ending cycle of financial difficulties, loans aren't always bad. Responsible borrowing, coupled with diligent financial planning, can mitigate the risk of falling into debt traps and ensure sustainable financial health. When managed wisely, loans can help individuals improve their financial situations and achieve long-term stability.

Not all debts are created equal. While high-interest consumer debts can pose significant challenges, strategic borrowing for investment or asset acquisition can yield substantial returns and enhance overall financial well-being.

Reason Why Taking a Loan Can Be Wise Decision

Below are some reasons why taking a loan can be a prudent decision:

One of the primary benefits of taking a loan is the ability to leverage financial opportunities that may not be feasible with existing capital. Thus, taking out a loan provides access to much-needed capital, enabling individuals to pursue opportunities that would otherwise be out of reach. Whether it's purchasing new gadgets, or renovating a home, loans provide individuals with the necessary funds to seize opportunities that they were limited to. Loans can also be helpful when you are on a tight budget and unexpected expenses arise. Overall, a loan gives you access to capital and empowers you to take control of your financial situation when you're in need.

In both personal and business finance, managing cash flow is paramount to sustainability and growth. Loans can serve as a valuable tool in optimizing cash flow. They can be useful for both individuals and businesses when they need extra cash, whether it's to get through tough times or take advantage of exciting opportunities, without using up all their savings. However, it's important to borrow responsibly and ensure that loan repayments fit into your budget. By using loans strategically, you can smooth out cash flow fluctuations and maintain financial stability.

Life is inherently unpredictable, and unexpected expenses can arise when least expected. Loans come in handy during emergencies or unexpected situations, allowing people to cover urgent expenses without using up their savings or taking extreme actions. This helps individuals address immediate financial needs while preserving their funds for other planned purposes. Whether it's covering medical bills, repairing a vehicle, or dealing with a sudden loss of income, having access to a loan can prevent individuals from dipping into savings.

In conclusion, while the decision to take out a loan may seem daunting, it's important to recognize the potential benefits and eliminate common myths surrounding loans. By understanding the dynamics of loans, and leveraging borrowed funds responsibly, individuals can harness the power of loans to achieve their goals and secure financial stability.

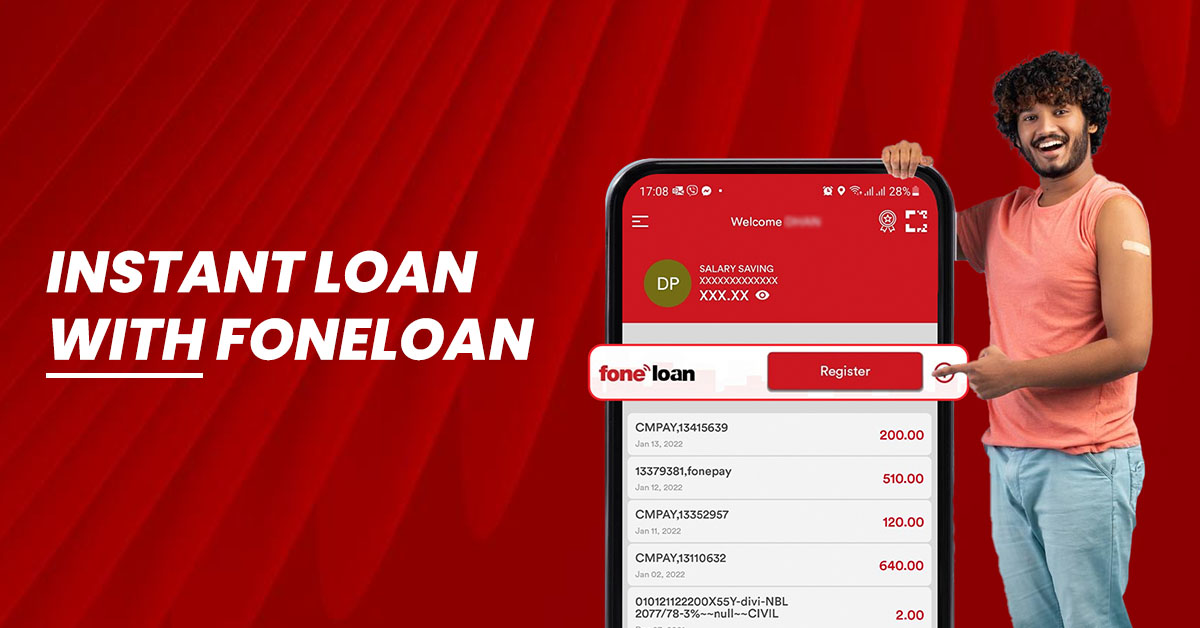

While we have briefly discussed the advantages of taking the loan, the application process involved in the process for a loan is very tedious in the context of Nepal. However, Foneloan eliminates all the hassle involved in the loan application process. With Foneloan, one can get instant access to a loan up to Rs. 2 lakh within just a few clicks from your mobile banking app. However, Foneloan is only available to the salary account. No more waiting in long queues or dealing with endless paperwork; Foneloan simplifies the process, ensuring you have the funds you need when facing unexpected financial challenges. Whether it's covering medical expenses, repairing your home, or managing any other urgent financial need, Foneloan offers a hassle-free solution.

Still have queries?